How to Discuss Cost and Coverage before Filling a Prescription

Dec, 10 2025

Dec, 10 2025

Imagine this: you leave your doctor’s office with a new prescription, feeling hopeful about your treatment. But when you get to the pharmacy, the pharmacist tells you the copay is $350. You didn’t expect that. You didn’t even know it was possible. So you leave the prescription on the counter and go home. That’s not rare. In fact, 22% of people skip filling prescriptions because of cost, according to 2023 GoodRx data. And it’s not just about being broke-it’s about not knowing what you’ll pay until it’s too late.

Why Talking About Cost Before the Prescription Matters

You wouldn’t buy a car without checking the price tag. So why do so many people accept a prescription without asking how much it’ll cost? The truth is, most patients assume their insurance will cover it-or they’re too embarrassed to ask. But here’s the thing: your doctor and pharmacist are there to help you, not surprise you. The real problem? Cost surprises happen because coverage details are buried in fine print. Insurance plans have formularies-lists of drugs they cover-and those lists change every year. Even if you’ve been on the same medication for years, your plan might suddenly stop covering it, or bump it to a higher tier with a much bigger copay. That’s why talking about cost before your doctor writes the script is no longer optional. It’s a standard part of patient care. The American Medical Association has recommended it since 2018. And starting in 2025, Medicare will cap out-of-pocket drug costs at $2,000 a year. That’s a big win-but only if you know how to use it.What to Ask Your Doctor Before They Write the Script

Don’t wait until you’re at the pharmacy. Bring up cost during your appointment. Here’s exactly what to say and what to ask:- “Is there a generic version of this drug?” Generics work the same as brand names but cost a fraction. For example, a brand-name blood pressure pill might cost $120 a month. The generic? $8.

- “Is this drug on my insurance’s formulary?” If it’s not, your plan won’t cover it-or will charge you way more. Ask your doctor to check before prescribing.

- “Are there other medications that work just as well but cost less?” Sometimes, switching to a different drug in the same class saves hundreds. For instance, if you’re on a specialty drug for arthritis, there might be a Tier 2 alternative with the same effect.

- “Will I hit my deductible soon? Should I wait until later in the year to fill this?” If you haven’t met your deductible yet, you’ll pay full price until you do. That could mean $500 out of pocket for one script. Waiting a few weeks might save you money.

- “Do you have samples or coupons?” Many doctors keep free samples on hand. Even if they don’t, they can often send you a manufacturer coupon that cuts the cost by 50% or more.

Know Your Insurance Plan Inside Out

You don’t need to be an expert, but you do need to know the basics of your plan. Here’s how to break it down:- Tiers: Most plans sort drugs into tiers. Tier 1 (generics) usually costs $5-$15. Tier 2 (preferred brands) is $25-$50. Tier 3 (non-preferred brands) can be $50-$100. Specialty drugs? They’re Tier 4 or 5-and can cost $200+ per month.

- Deductibles: If you haven’t met your deductible, you pay full price. In 2023, the average individual marketplace deductible was $480. That means if your drug costs $300 and you’ve only paid $100 toward your deductible, you pay the full $300.

- Copay vs. Coinsurance: A copay is a fixed amount (like $30). Coinsurance is a percentage (like 30% of the drug’s cost). Coinsurance can be dangerous-if your drug costs $1,000, 30% is $300. That’s not a copay. That’s a bill.

- Annual limits: Medicare Part D has a hard cap of $2,000 out-of-pocket in 2025. Commercial plans? Most have no cap. You could pay thousands in a year.

Use These Tools Before You Walk Into the Pharmacy

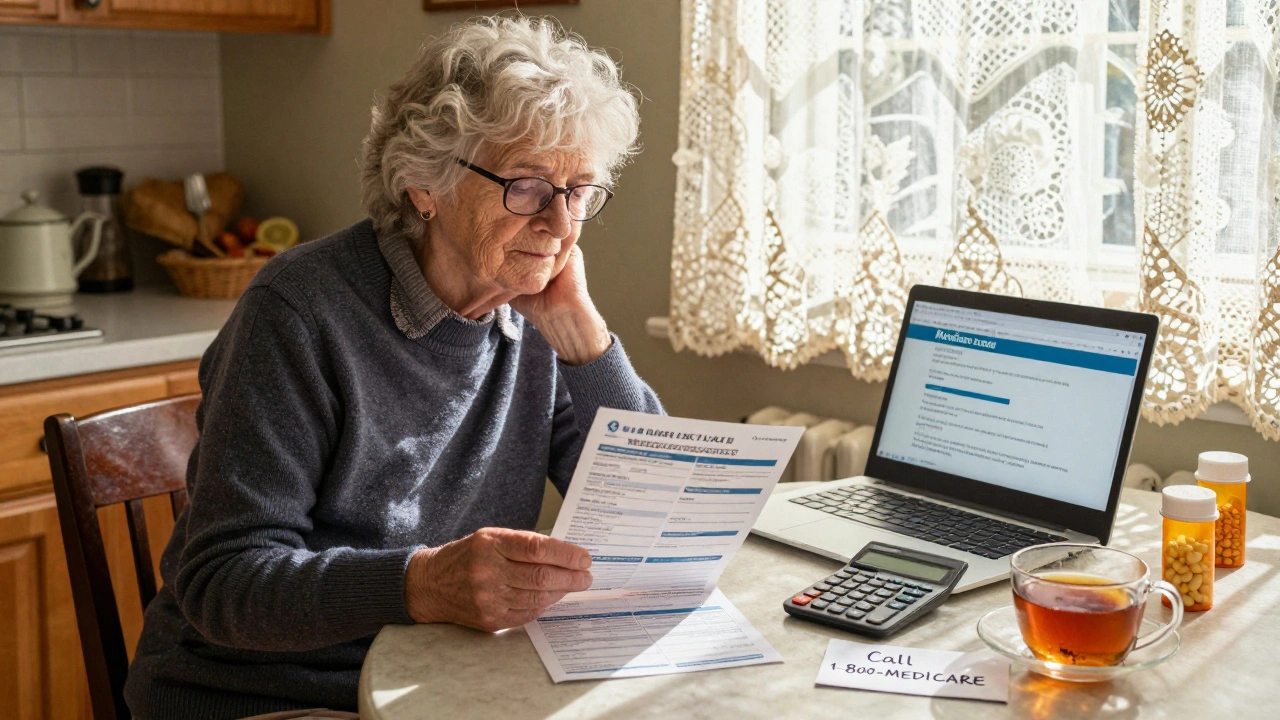

You don’t have to guess. There are free tools that show you exactly what you’ll pay:- Medicare.gov Plan Finder: If you’re on Medicare, use this every October. It lets you compare costs for your exact medications across all Part D plans for the next year. It’s updated every October 1st.

- GoodRx: Enter your drug name and zip code. It shows you the lowest cash price at nearby pharmacies-and sometimes it’s cheaper than your insurance copay. One user saved $287 on blood pressure meds by showing the pharmacist a GoodRx price.

- CVS Caremark’s Check Drug Cost Tool: If your plan uses CVS Caremark, use their online tool. It tells you your exact copay, if there’s a generic, and if mail-order is cheaper.

- Call your insurer: Have your drug’s NDC number (found on the bottle) ready. Call customer service. Ask: “What’s my out-of-pocket cost for this drug right now?” Don’t trust what you see online-call.

What If the Drug Isn’t Covered?

If your doctor prescribes something your plan doesn’t cover, don’t panic. You have options:- Ask for prior authorization: Your doctor can submit a request to your insurer explaining why this drug is necessary. About 68% of specialty drugs need this, and it often works.

- Request a formulary exception: If your drug is medically necessary but not on the list, your doctor can appeal. The Patient Advocate Foundation says 68% of these appeals are approved when the doctor provides clinical evidence.

- Use patient assistance programs: Drug makers often offer free or low-cost meds to people who qualify based on income. Check NeedyMeds.org or the manufacturer’s website.

Special Cases: Insulin and Specialty Drugs

Insulin is different. Since 2023, Medicare beneficiaries pay no more than $35 per month for covered insulin. That’s a federal law. But if you’re on a commercial plan, you might still pay $100+ unless your plan has its own cap. Ask your doctor to prescribe insulin with a $35 cap-and confirm it’s covered. Specialty drugs (for conditions like MS, rheumatoid arthritis, or cancer) are the most expensive. They often cost $1,000+ per month. But here’s the thing: 68% of them require prior authorization. That means your doctor has to jump through hoops just to get you the drug you need. Don’t wait until the last minute. Start the process early. Ask your doctor to submit the paperwork during your visit.

The New Medicare Payment Plan (2025)

Starting in 2025, Medicare Part D will introduce a new option: the Medicare Prescription Payment Plan. Instead of paying your full copay at the pharmacy, you can pay in monthly installments-capped at $2,100 a year. That’s huge. But here’s the catch: you have to enroll before September. If you wait until October, there won’t be enough months left to spread the payments. If you’re on Medicare and take a high-cost drug, this plan could save you from a financial shock. Talk to your pharmacist or call 1-800-MEDICARE to ask if you qualify.What to Do If You’re Still Stuck

Sometimes, even after all the checks, the cost is still too high. That’s when you need backup:- Call your doctor’s office again. Ask if they have a financial counselor. Many clinics do.

- Use Patient Advocate Foundation. They help people navigate insurance denials and find aid programs. Their helpline is free.

- Check local pharmacies. Some independent pharmacies offer discount programs for cash-paying customers.

- Don’t skip doses. Research shows patients who skip doses due to cost are 37% more likely to end up in the hospital. That’s more expensive than the drug.

It’s not your fault if you didn’t know this stuff. The system is confusing. But now you do. And that changes everything.

What should I do if my insurance denies coverage for my prescription?

Don’t accept the denial right away. Ask your doctor to file a prior authorization or formulary exception. Provide medical records showing why the drug is necessary. About two-thirds of these appeals succeed when supported by clinical evidence. You can also call your insurer’s appeals line and ask for a written explanation of the denial.

Can I use GoodRx even if I have insurance?

Yes. GoodRx often shows lower prices than your insurance copay, especially for generic drugs. At checkout, tell the pharmacist you want to use the GoodRx price instead of your insurance. You can’t combine them, but you can choose the cheaper option. Many people save hundreds this way.

Why does my prescription cost more at some pharmacies than others?

Pharmacies set their own cash prices, even for insured patients. A drug might cost $120 at CVS but $45 at Walmart or Walgreens. Use GoodRx or call ahead to compare. Mail-order pharmacies often offer the lowest prices for long-term medications.

Does the Inflation Reduction Act help people with private insurance?

Not directly. The $2,000 out-of-pocket cap and $35 insulin rule apply only to Medicare Part D. But some private insurers have started matching these limits to stay competitive. Ask your plan if they’ve adopted similar caps. You might be surprised.

When is the best time of year to fill expensive prescriptions?

If you haven’t met your deductible yet, waiting until later in the year can save money. Most people meet their deductible by August or September. Filling a $500 drug in November means you pay nothing if your deductible’s already met. But don’t delay if the medication is urgent.

How do I know if my doctor uses Real-Time Prescription Benefit tools?

Ask directly: “Can you check my drug coverage right now using your computer?” If your doctor uses an electronic health record system like Epic or Cerner, they likely have access to tools like Surescripts’ RTPB. These show your exact copay before the script is printed. If they say no, ask them to call your insurer for a quote during your visit.

Are there programs to help pay for specialty drugs?

Yes. Most drug manufacturers offer patient assistance programs for high-cost medications. You can apply online using your income information. Programs like NeedyMeds.org or RxAssist.org list them all. Some cover 100% of the cost for low-income patients.

Vivian Amadi

December 10, 2025 AT 22:57This article is literally life-saving. I once walked out of a pharmacy with a $420 insulin bill and cried in my car. No one told me about GoodRx. No one. My doctor just handed me the script like it was a coupon for coffee. Shame on the system.

And don't even get me started on how pharmacies jack up cash prices just to make you feel desperate. I paid $110 at CVS. Walked two blocks to Walgreens. $37. Same drug. Same bottle. Same poison.

Stop acting like this is normal. It's not. It's predatory.

Also-why the hell are we still talking about 'formularies'? Just say 'what drugs does my plan hate today?' It's clearer.

And yes, I called my insurer. They put me on hold for 22 minutes. Then said 'check your portal.' My portal is a glitchy nightmare. I need a human. Not a bot that says 'thank you for your patience.' I'm not patient. I'm broke.

Taylor Dressler

December 12, 2025 AT 10:51Great breakdown. I want to add one thing that’s often overlooked: when you ask your doctor about alternatives, always specify ‘I need something that works for my kidney function’ or ‘I can’t take anything that interacts with my statin.’ Many doctors don’t know your full med list unless you remind them.

Also, if you’re on Medicare, the $2,000 cap applies only after you hit the catastrophic threshold. You still pay 5% until then. Don’t assume you’re safe until you’re past $7,410 in total drug costs. Use the Medicare Plan Finder every October-don’t wait until January. Changes are finalized then.

And yes, GoodRx works even if you have insurance. Just tell the pharmacist you’re paying cash. They’re legally required to give you the lower price. Most don’t know that. Be polite but firm.

This isn’t about being ‘difficult.’ It’s about being informed. You’re not asking for a favor. You’re exercising your right as a patient.

Courtney Blake

December 13, 2025 AT 12:50Ugh. Another ‘just ask your doctor’ article. Like that’s the solution. My doctor’s office has a 3-week wait for a non-urgent visit. I need my med NOW. And when I finally get in, they’re rushing because they have 12 more patients.

And don’t get me started on ‘prior authorization.’ I’ve had to fax 3 forms, wait 4 days, call 5 times, and then get denied because ‘another drug is preferred.’ Preferred? By who? The insurance CEO? My doctor wrote ‘medically necessary’ in ALL CAPS. Still denied.

So now I’m paying $600/month out of pocket because the system is designed to break people. And you want me to ‘be proactive’? Nah. I’m done.

😂

Sylvia Frenzel

December 13, 2025 AT 23:44Why do these articles always assume everyone has internet, a phone, and the energy to fight? I work two jobs. I have three kids. I don’t have time to call insurers or compare pharmacy prices. I just need the damn pill.

And no, I can’t ‘wait until later in the year’ to fill my antidepressant. I don’t have a ‘later.’ I have today. And today, I’m choosing between food and meds.

This isn’t advice. It’s a luxury.

And yes, I know about GoodRx. I tried it. The pharmacy said ‘we don’t honor that.’ So what now? I just stop taking it?

They should just make meds cheap. Not make us jump through hoops like circus animals.

Lisa Stringfellow

December 14, 2025 AT 15:11Wow. So now we’re blaming patients for not being healthcare experts? That’s rich.

You think I want to memorize tiers, formularies, and NDC codes? I’m not a pharmacist. I’m a single mom who works nights. I don’t have time to ‘use tools.’

And let’s be real-most doctors don’t even use those ‘real-time benefit tools.’ I asked mine. They said ‘we don’t have that system.’ So what’s the point of this whole article?

It’s not about knowledge. It’s about power. And we don’t have any.

Just fix the system. Not our behavior.

Eddie Bennett

December 16, 2025 AT 07:55I’ve been there. I had to choose between my asthma inhaler and my daughter’s school lunch money last year.

But here’s what changed things for me: I started asking my pharmacist, ‘What’s the cash price?’ before I even mention insurance. Most of the time, it’s cheaper. I’ve saved over $1,200 in a year just by doing that.

Also, don’t be afraid to say ‘I can’t afford this.’ Doctors aren’t mad. They’re relieved. They want you to take your meds. They’re not there to shame you.

And if you’re on Medicare, call 1-800-MEDICARE. The reps are actually helpful. They’ll walk you through the payment plan. I did it while crying in my car. No judgment. Just help.

You’re not alone. And you’re not failing. The system is.

john damon

December 17, 2025 AT 00:43bro i just use goodrx + coupons + my dog’s name as a fake patient ID and i get my meds for $3 😎

also if you say ‘my insurance denied it’ they give you free samples. just say it with confidence. they don’t check. trust me.

also if you’re on insulin, just ask for the $35 version. they’ll give it to you even if you’re not on medicare. i did it. no one asked questions.

you’re welcome 🐶

Monica Evan

December 18, 2025 AT 13:06OMG I JUST REALIZED I’VE BEEN PAYING $180 FOR MY DIABETES MED BECAUSE I THOUGHT INSURANCE WAS COVERING IT 😭

WENT TO WALMART WITH GOODRX-$12. SAME DRUG. SAME EXPIRATION DATE.

MY DOCTOR NEVER TOLD ME. NO ONE DID. I FELT SO STUPID.

SO NOW I ASK EVERY TIME: ‘WHAT’S THE CASH PRICE?’

AND I TELL PHARMACISTS ‘I’M PAYING CASH’ EVEN IF I HAVE INSURANCE.

IT’S NOT SHAMEFUL. IT’S SMART.

AND IF YOU’RE STRUGGLING? TEXT ME. I’LL HELP YOU FIND THE CHEAPEST PLACE. NO JUDGMENT. WE’RE ALL JUST TRYING TO SURVIVE.

❤️

Aidan Stacey

December 19, 2025 AT 11:32Let me tell you about my cousin. She had MS. Her drug cost $14,000 a month. Insurance denied it. She filed a formulary exception. Got approved. But it took 90 days. She was in a wheelchair for three months because she couldn’t afford to buy it out of pocket.

That’s not healthcare. That’s torture.

But here’s the thing-when she finally got it, she started a nonprofit to help others navigate this mess. Now she helps 200 people a year. She didn’t wait for someone to fix it. She fixed it herself.

You don’t need to be a hero. Just be brave enough to ask. One question can change your life.

And if you’re scared? Say it out loud: ‘I can’t afford this.’

That’s not weakness. That’s the first step to power.

Katherine Liu-Bevan

December 20, 2025 AT 18:50One thing the article doesn’t mention: many pharmacies offer loyalty programs for cash customers. At Rite Aid, you can join their wellness program and get $10 off your next prescription every time you spend $50. It adds up.

Also, if you’re on a commercial plan, ask if your insurer has a ‘preferred pharmacy network.’ Sometimes, using a specific pharmacy cuts your copay by 50%.

And if you’re on insulin-don’t assume your plan covers the $35 version. Call them. Ask: ‘Do you cover the $35 insulin under the Inflation Reduction Act?’ If they say no, ask for a supervisor. Most don’t know the law.

This isn’t rocket science. It’s just a checklist. Write it down. Keep it on your fridge.

Paul Dixon

December 21, 2025 AT 01:07Man, I used to think this stuff was just for rich people. Then I got diagnosed with high blood pressure. My first script was $380. I cried. My wife cried. We didn’t eat for a week.

Then I found GoodRx. Found the generic. $8. I felt like a genius.

Now I tell everyone: if you’re on meds, ask for the cash price before you let them swipe your card. It’s not rude. It’s smart.

And if your doctor looks at you weird? Just say, ‘I’m trying to be responsible.’ They’ll get it.

We’re all just trying to stay alive. No shame in that.

Jimmy Kärnfeldt

December 22, 2025 AT 10:53There’s a quiet revolution happening here. It’s not in the halls of Congress. It’s in the pharmacy aisles. People are finally realizing: we don’t have to be passive. We can ask. We can compare. We can say no.

It’s not about being ‘difficult.’ It’s about being human.

And the more people who do this, the more the system has to change.

I used to think I was alone. Now I know I’m part of a movement.

So go ahead. Ask your doctor. Call your insurer. Use GoodRx. Walk into that pharmacy like you own it-because you do.

You’re not a patient. You’re a person. And your health isn’t a commodity.

It’s yours.

Ariel Nichole

December 22, 2025 AT 15:51I’ve been on the same medication for 8 years. Last year, my copay jumped from $15 to $140. I didn’t know why. I just paid it.

Then I found out my plan changed the tier. No one told me.

So now I check my plan’s formulary every January. It takes 10 minutes. I save $1,500 a year.

It’s not hard. You just have to care enough to look.

And if you’re overwhelmed? Start with one thing. Ask for the cash price. That’s it. One step. That’s how change starts.

matthew dendle

December 24, 2025 AT 02:30lol so you just gotta be a superhero to get your meds? ask ask ask. call call call. check check check. bro i got a 9 to 5 and 2 kids. i dont got time to be a healthcare detective.

and if your doctor says they use real time tools but they dont? then what? you gonna sue em? nah.

the real solution? make drugs cheap. not make us jump through 17 hoops.

but hey. keep telling people to ‘be proactive.’ that’ll fix it. 😂